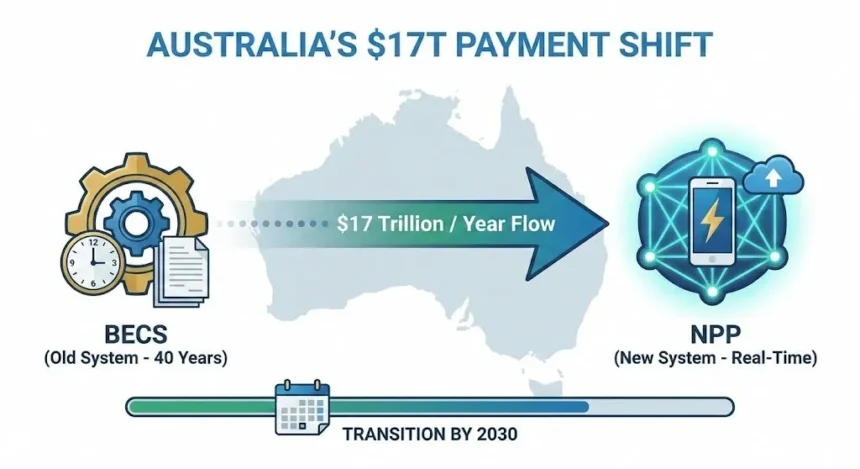

The BECS framework that processes 90% of Australia’s account-to-account payments is set for decommissioning by 2030. Here’s what the numbers actually say about where the money is moving.

Most Australians have never heard of BECS. That’s the Bulk Electronic Clearing System — the backend plumbing that has quietly shuffled wages into bank accounts, pulled direct debits for electricity bills, and moved pension payments every fortnight since the late 1980s. It handles roughly 3.5 billion transactions a year, worth north of $17 trillion. And AusPayNet wants it gone by 2030.

The replacement is already running. The New Payments Platform, or NPP, processed 1.6 billion transactions in 2024 alone, totalling AU$1.99 trillion — a 23% jump on the year before, according to Australian Payments Plus. That sounds enormous until you realise BECS still carries almost 90% of all retail account-to-account payment value. The gap between what the NPP handles today and what it needs to absorb by decade’s end is considerable.

How BECS works and why it is being retired?

BECS runs on batch processing. Payments get bundled into files, shipped between banks during business hours, and settled in lumps. A payment made late on a Friday might not land until the following week. The messaging format shares barely any data, which makes reconciliation difficult for businesses and complicates fraud detection.

The Reserve Bank of Australia flagged these shortcomings years ago. In a December 2024 speech at the AusPayNet Summit, RBA Assistant Governor Brad Jones discussed the BECS-to-NPP transition and pointed out that BECS still underpins payroll, welfare, and pension payments that millions of Australians depend on. The Payments System Board commissioned a formal risk assessment of the decommissioning, which reported back in early 2025.

The NPP works differently. Every transaction settles individually, in real time, around the clock. It supports richer data — up to 280 characters per payment description — which means businesses can automate matching and reconciliation instead of doing it by hand. The per-transaction cost at the wholesale level has dropped from $0.39 in 2019 to roughly $0.04 by FY25, according to AP+. That cost keeps falling as volumes climb.

PayID registration growth across Australia

PayID is the bit of the NPP that most people actually interact with. Instead of typing in a BSB and account number, you link your phone number or email to your bank account. Someone sends money to that alias, it arrives in seconds.

The adoption curve has been sharp. A few numbers worth noting.

- By 2024, there were over 18.5 million registered PayIDs across Australia, per Australian Payments Plus data.

- Wikipedia’s NPP entry, updated April 2025, puts the figure at over 25 million.

- Payments CMI estimated registrations had passed 27 million by mid-2025.

- More than 110 banks and credit unions now support the system.

- Over 114 million accounts were enabled to send or receive NPP payments by late 2024.

Australia’s adult population sits at around 20 million. So the registration count exceeding 25 million means plenty of people hold multiple PayIDs — a work one, a personal one, maybe one tied to a side business. That kind of redundancy tends to signal genuine daily use rather than people signing up once and forgetting about it.

Hellozai’s 2025 payments report noted that around one in three Australians had used PayID for personal transfers by 2023, and that figure has kept climbing as more banking apps bake it into their default payment flows. The weekly usage rate sat at 47% among registered users, based on research NPP Australia conducted.

Cash usage decline and mobile wallet adoption

The broader context here matters. Cash accounted for roughly 70% of all Australian payments back in 2007. The RBA’s 2022 Consumer Payments Survey put that at 16% for in-person transactions — and some analysts reckon it sat closer to 11-12% by 2024. The RBA itself has projected that cash could drop to 4% of transactions by 2030.

ATM withdrawals tell the same story from a different angle. Monthly withdrawals have fallen from about 75 million at their peak to under 28 million. The number of ATMs has shrunk by over a quarter since late 2016, mostly bank-owned machines disappearing.

Meanwhile, mobile wallets have gone the other direction entirely. Fresh data from December 2024 showed that 44% of device-present transactions in Australia were made through Apple Pay, Google Pay, or Samsung Pay, with 54% still on contactless cards and a tiny 2% using card-insert. The Australian Banking Association reported that mobile wallet transactions hit AU$126 billion in annual value during 2024, nearly doubling year on year. Industry forecasts from GlobalData project that the figure could clear AU$200 billion by the end of 2025.

Mordor Intelligence valued Australia’s total payments market at USD $1.07 trillion in 2025, with projections pushing it to USD $2.29 trillion by 2030 at a compound annual growth rate of 16.44%. Internet penetration sits at 96%. Smartphone ownership is effectively universal in urban areas.

How the credit card gambling ban shifted payment methods

One of the clearer illustrations of how quickly PayID adoption can move came from online gambling regulation.

On 11 June 2024, Australia’s credit card gambling ban took effect under the Interactive Gambling Amendment (Credit and Other Measures) Bill. The rules are straightforward: licensed wagering operators cannot accept credit cards, credit-linked digital wallets, or cryptocurrency for deposits. The Australian Communications and Media Authority oversees compliance, and fines run up to $247,500 per breach. Betchoice has already been fined AU$1 million. Ultrabet and PointsBet accepted 18-month undertakings with external audits.

The ban forced every operator to rebuild their payment infrastructure around debit-based methods. PayID became the default for a lot of them, because it is instant, doesn’t require sharing BSB details, and works with the banking apps people already have on their phones. Across sectors like PayID pokies and sports wagering platforms, the shift was measurable almost immediately — players who had been using Visa credit simply moved to PayID-linked bank transfers.

Online gambling turnover had already surged 165.7% to AU$75.4 billion in the 2022-23 financial year, representing 31% of Australia’s total gambling market. That volume of money needing to move through compliant channels put real pressure on the NPP’s throughput. The BetStop National Self-Exclusion Register, which integrates with banking infrastructure, recorded nearly 45,000 active exclusions by mid-2025 — up from 22,000 at its April 2024 launch.

The gambling sector is one example, but it is a useful one because the regulatory deadline was hard and the transition was fast. E-commerce refunds, gig economy payouts, subscription billing — they are all moving toward real-time settlement too, just without the same kind of forcing function.

Remaining gaps before the 2030 deadline

The NPP currently handles around a third of account-to-account payments. That means roughly 70% of A2A volume — the bulk of payroll processing, pension disbursements, supplier payments, and government transfers — still runs through BECS. Getting all of that across in four-odd years is not straightforward.

AP+ has identified a few specific problems that need solving.

- Bulk payment handling. BECS was built for batch files. The NPP processes individual transactions. AP+ is developing a multi-credit transfer message format that bundles multiple payments into a single NPP message, which went into detailed design during 2025.

- Account reach. Some banks connected to BECS have not joined the NPP yet. Even among those that have, not all BECS-reachable accounts can currently receive NPP payments. Every single one needs to be reachable before BECS can actually switch off.

- Capacity. The NPP completed a capacity uplift in December 2023 and has another scheduled for December 2025. AP+ says the platform can already handle double its current volumes, but BECS processes more than double what the NPP does today.

- Cost clarity. BECS is cheap because it is old and fully depreciated. The NPP’s per-transaction cost is falling, but businesses need to weigh that against efficiency savings — less manual reconciliation, fewer failed payments, instant confirmation.

PayTo is the other piece. It launched for billers in 2024 as a modern replacement for direct debits, letting businesses initiate real-time payments from customer accounts after digital authorisation. It replaces paper-based direct debit forms and gives both sides more visibility over recurring payments. Adoption is still early, but analysts expect it to pick up through 2025 as more banks and software providers integrate it.

Confirmation of Payee — a feature that checks whether the name on the account matches the details entered before the payment goes through — was scheduled for phased rollout through 2024-2025. It is meant to cut down on both scams and misdirected payments. PayID has been flagged as a vehicle for marketplace scams, and adding name verification is one of the more practical defences available.

Where this leaves Australia’s payment infrastructure

Australia’s payments system is being rebuilt from the ground up, and most of the people whose money flows through it barely notice. The NPP was built to sit underneath existing banking apps, not to become its own consumer brand. PayID is the closest thing to a public-facing identity the system has, and even that just feels like sending money to a phone number for most users.

The 2030 deadline gives the whole thing a hard edge, though. Brad Jones at the RBA compared it to the shutdown of analogue TV in 2013 — a transition everyone knew was coming, but one that still required coordination across dozens of institutions and millions of end users. The payments version involves $17 trillion in annual flows and touches every employer, every pension recipient, every direct debit arrangement in the country.

Whether the industry hits that target or needs an extension remains open. The RBA’s risk assessment surfaced concerns about readiness, and Jones himself noted that all stakeholders need a voice and that time is of the essence. What is not in doubt is the direction. Real-time, data-rich, always-on payments are where Australia is headed. The batch-processing era that began in the late 1980s is winding down, and the infrastructure replacing it is already carrying nearly $2 trillion a year.