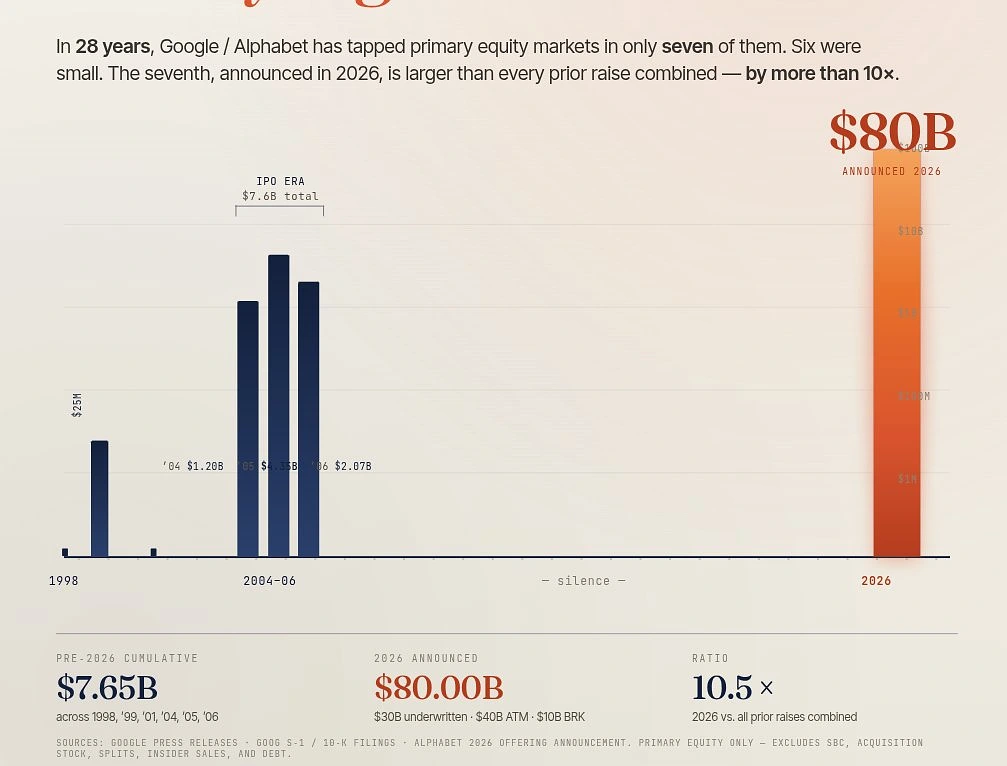

$80 billion. That’s what Alphabet just pulled together — and the structure of how it did that is worth actually reading.

Three parts: a $30 billion public offering (split between $15 billion in mandatory convertible preferred stock and $15 billion in Class A and Class C shares), a $40 billion at-the-market program kicking off in Q3 2026 that lets the company sell shares on an ongoing basis, and a $10 billion private placement from Berkshire Hathaway — $5 billion in Class A shares at $351.81 and $5 billion in Class C at $348.20. Berkshire, now run by Greg Abel since Buffett stepped down at the end of 2025, had already tripled its Alphabet stake in Q1 this year. The private placement is the continuation of that, not a pivot.

Q1 2026 numbers were already strong before any of this — $109.9 billion in revenue, up 22% year-on-year, with 350 million paid subscribers across Google’s services (up from 325 million the previous quarter). The income picture isn’t the issue. The issue is what the next two years of infrastructure actually costs.

Alphabet updated its full-year 2026 capex guidance to $180–190 billion, climbing from the prior $175–185 billion range. Q1 alone came in at roughly $35.7 billion, nearly all of it technical infrastructure for AI. And 2027 is expected to go higher still. The $80 billion raise, per the official press release, is designed to fund investments “in a balanced way while retaining a healthy balance sheet” — proactive balance-sheet management, not a scramble. The company posted around $174 billion in operating cash flow over the trailing twelve months. This is about moving at a pace that quarterly earnings alone can’t sustain.