If you’ve ever walked into a corner shop in Karachi, Nairobi, or Dhaka, handed someone cash, and watched a digital balance appear on your phone seconds later — you’ve used an agent deposit network. You probably didn’t think twice about the backend. Cash went in, numbers went up, done.

But what actually happened between the moment you handed over that cash and the moment your digital balance changed?

That transaction passed through a ledger system, hit an API, got validated against a float balance, and settled in real time — all without touching a bank. The same architecture powers M-Pesa in Kenya, JazzCash and Easypaisa in Pakistan, bKash in Bangladesh, and platforms like 1xBet deposit agent networks that use human agents as local cash-in/cash-out points for users who can’t or won’t use traditional payment rails.

This is how all of it works under the hood.

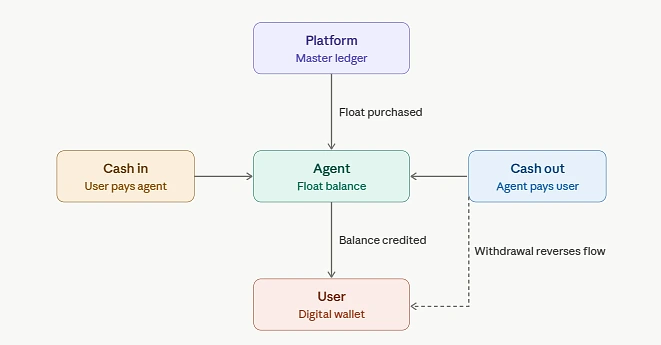

The Agent Isn’t a Payment Gateway — They’re a Float Node

First thing to understand — the agent at the shop counter is not processing your payment the way a card terminal does. A card terminal talks to a bank. The agent doesn’t.

So what are they doing?

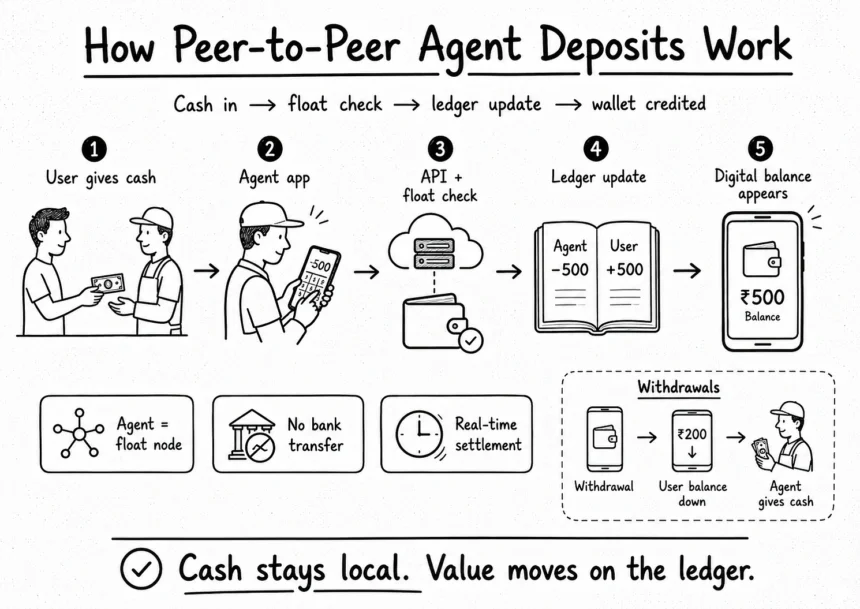

They’re operating on a pre-funded float. Before they can process a single deposit for anyone, they’ve already bought a block of digital credit from the platform. Think of it like buying phone top-up vouchers in bulk — except instead of selling airtime, they’re selling deposit credits into user accounts.

When you hand the agent cash:

- The agent doesn’t send your money anywhere

- They debit their own pre-funded float balance

- The platform credits your account from that float

- The agent keeps your cash as reimbursement for the float they just spent

No bank transfer happens. No card network gets involved. The entire transaction is an internal ledger adjustment between three parties — the platform, the agent, and you.

And withdrawals? Exact reverse.

You request a withdrawal through the app. The platform pulls the amount from your account, credits it back into the agent’s float, and the agent hands you cash. Their float goes up, your digital balance goes down.

How the API Layer Connects Everything

The agent isn’t typing numbers into a spreadsheet. They’re using a mobile app — and that app is talking to the platform’s backend through a RESTful API.

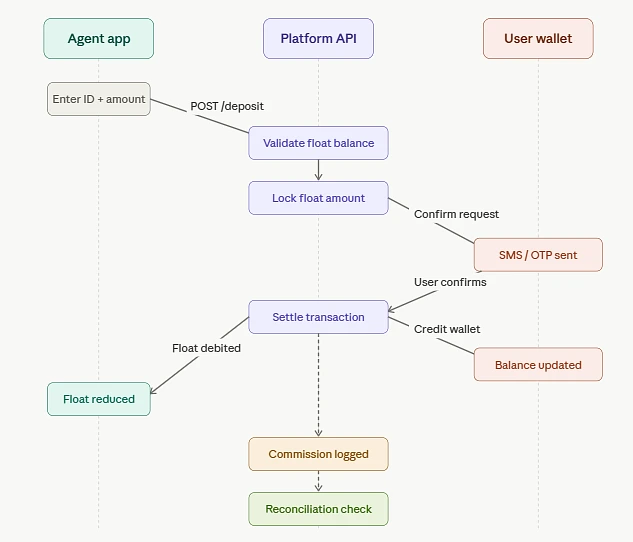

What happens when you walk up to an agent and say, “Deposit 5,000 into my account”?

Here’s the actual sequence:

- Agent opens the app, enters your user ID and the deposit amount

- The app sends a POST request to the platform’s transaction API

- The API checks the agent’s float balance — is there enough to cover 5,000?

- If yes, the system creates a pending transaction and locks the amount from the agent’s float

- You get a confirmation prompt — SMS, push notification, or in-app OTP, depending on the platform

- Once confirmed, the transaction settles. Your account goes up by 5,000, the agent’s float drops by 5,000, and the platform logs the whole thing with timestamps and transaction IDs

- The agent’s commission gets calculated and either added to their float or paid out on a schedule

If the float check fails at step 3 — not enough balance — the transaction dies right there. The agent sees an “insufficient float” error and has to top up before they can process anything else.

M-Pesa’s Daraja API handles this with a series of modular REST endpoints. Each part of the transaction — the initiation, the authorization, the settlement, the callback — runs through its own endpoint. The platform never exposes the full chain to the agent’s app. The app only sees what it needs to see: balance, transaction status, success or failure.

JazzCash and Easypaisa use a similar pattern in Pakistan. The agent’s SIM-based or app-based interface connects to a middleware layer that routes to the microfinance bank’s core ledger. The transaction model is identical — float pre-purchase, real-time debit/credit, commission calculation, and settlement.

The Ledger Structure Under All of This

Every agent deposit system runs on a double-entry ledger at its core. Not blockchain. Not some exotic distributed system. Plain double-entry bookkeeping — the same accounting structure that’s been around since the 1400s, just running on servers instead of paper.

What does the ledger actually track?

Three balances that have to stay in sync at all times:

- Platform master account — the total pool of digital currency in the system

- Agent float accounts — one per agent, showing how much deposit credit they currently hold

- User wallets — one per user, showing their available balance

Every single transaction creates two entries. A deposit creates a debit on the agent’s float and a credit on the user’s wallet. A withdrawal creates the opposite. The platform master account reconciles the total — all agent floats plus all user wallets should always equal the master pool.

If the numbers don’t match, something broke. And the platform’s reconciliation engine catches that within minutes, not days.

Why does this matter for the person handing over cash?

Because it means there’s a real-time audit trail for every transaction. Your deposit isn’t sitting in some agent’s pocket waiting to be forwarded. The ledger adjustment happens at the moment of confirmation. The agent can’t selectively “forget” a deposit because the platform has already logged it on both sides of the book.

Float Management Is Where Agents Succeed or Fail

The technology works. The APIs work. The ledger works. The part that actually breaks in practice is float management — and it’s almost entirely a human problem.

An agent in a busy area might process 200+ transactions a day. If deposits outpace withdrawals, their float drains fast. If withdrawals outpace deposits, they end up sitting on too much cash and not enough digital float to process incoming deposit requests. Either way, they’re stuck.

M-Pesa agents in rural Kenya have to make physical trips to banks to rebalance their float. That costs time and transport money. JazzCash and Easypaisa agents in Pakistan face the same problem — 96% of agents in Pakistan are running parallel businesses, and 78% serve multiple providers simultaneously. They’re splitting a limited float budget across JazzCash, Easypaisa, and sometimes a third platform, and whoever has the highest transaction demand on a given day wins most of that float.

What does rebalancing look like technically?

The agent transfers cash to a designated bank account or super-agent, and the platform’s backend converts that into float credit. Some platforms handle this through USSD codes. Others have built it directly into the agent app — the agent initiates a bank transfer, the platform’s webhook picks up the confirmation from the bank’s API, and the float gets topped up automatically.

The more sophisticated platforms run predictive float management tools that estimate an agent’s daily transaction volume and prompt them to rebalance before they run dry. That’s a data science layer sitting on top of the same ledger infrastructure — transaction history analysis, time-of-day patterns, day-of-week cycles, seasonal spikes.

Where Online Platforms Adopted the Same Model

This isn’t just a mobile money thing anymore. The agent deposit model has spread to any platform that needs to serve users in cash-heavy economies where card penetration is low and bank transfers are slow or restricted.

Online gaming and betting platforms figured this out early. In markets across South Asia, Africa, and parts of Southeast Asia, formal payment methods either don’t work reliably or aren’t available to a large portion of the user base. The solution was the same one M-Pesa pioneered — put a human agent between the cash and the platform.

The 1xBet deposit agent network is a direct application of this architecture. An agent pre-purchases float from the platform, takes cash from a user, enters their gaming account ID in the agent app, and the platform credits the account in real time. The transaction flow, the float logic, the API sequence, the ledger entries — structurally identical to what happens at a JazzCash agent counter.

The tech isn’t new. The application is.

The Transaction Flow — Step by Step

Here’s the entire lifecycle of a single agent-processed deposit, from cash-in to settled balance:

| Step | What Happens | Who’s Involved |

| 1 | Agent pre-purchases float from platform | Agent → Platform |

| 2 | User approaches agent with cash | User → Agent |

| 3 | Agent enters user ID + amount in app | Agent app → Platform API |

| 4 | API validates agent float balance | Platform backend |

| 5 | System creates pending transaction, locks float | Platform ledger |

| 6 | User receives confirmation prompt (SMS/OTP) | Platform → User |

| 7 | User confirms — transaction settles | Platform ledger finalises |

| 8 | User balance increases, agent float decreases | Double-entry recorded |

| 9 | Commission calculated and credited to agent | Platform → Agent |

| 10 | Platform reconciliation engine verifies totals | Platform backend |

The whole thing takes between 5 and 30 seconds depending on network latency and confirmation method.

What This Architecture Gets Right — and Where It Breaks

What works:

It bypasses banks entirely for the end user. No card number, no IBAN, no waiting two business days for a transfer to clear. The settlement is instant because it’s an internal ledger move, not an interbank transaction. The agent network scales horizontally — add more agents, serve more users, no infrastructure buildout required.

Where it breaks:

Float liquidity is the single biggest pain point. An agent who runs out of float at 6pm on a Friday is useless until Monday morning when the bank opens. Agent fraud is a risk — though the real-time ledger limits the window for it. And in unregulated markets, there’s no consumer protection layer. If the platform goes down or disappears, the user’s balance goes with it.

The technology underneath is solid. It’s been proven at scale across dozens of countries and hundreds of millions of users. The weak points are almost always operational — humans running out of cash, humans mismanaging float, platforms cutting corners on reconciliation. The API layer doesn’t break. The agent’s wallet does.