In late 2025 there are over 3700+ data centers in the US, and between 2026 and 2035 ABI Research expects another 3,226 to be built worldwide. The US leads the world by a massive margin, second-placed UK has just 484. And somehow it’s still not enough.

According to Goldman Sachs there is a current capacity shortage of roughly 11 gigawatts, which is the electricity for about 7.5 million homes. Vacancy rates fell to record lows of 3% in 2025. And the 2026 Global Data Center Outlook JLL published just days ago says nearly 100 GW of new capacity has to come online between now and 2030 just to keep up with demand.

That would double current global capacity.

So the US has the most data centers anywhere in the world, and still a deficit measured in gigawatts. The question for anyone renting server infrastructure, then, is what all of that actually does to cost, availability, and where the smart money goes.

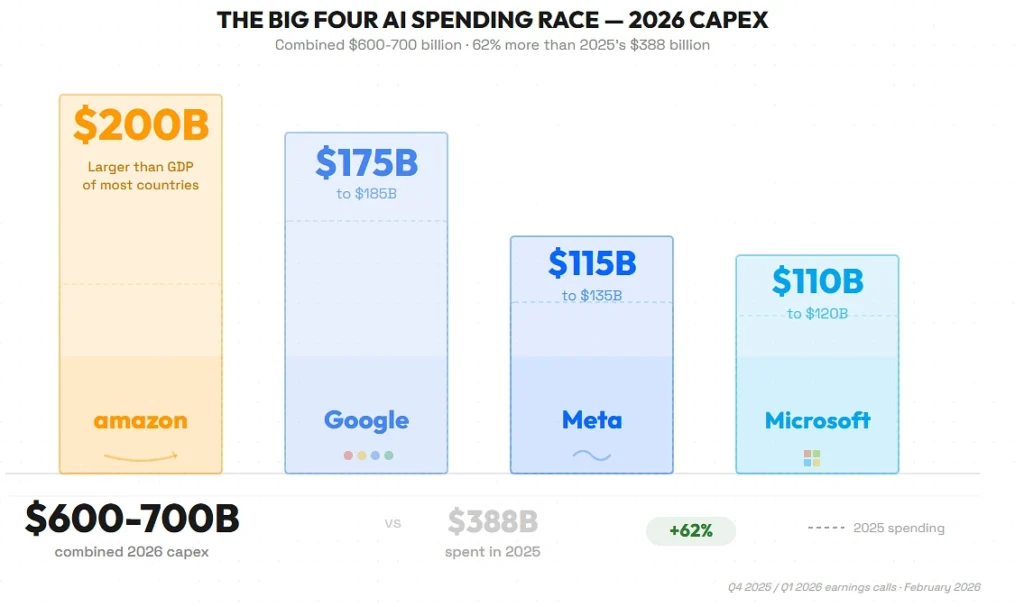

$630 billion in hyperscaler spending and 26% of projects still delayed

During their earnings calls in early February, the Big Four (Amazon, Google, Meta and Microsoft) announced they collectively expect to spend between $600 billion and $700 billion on capital expenditure in 2026, a 62% jump from the $388 billion they spent in 2025. The breakdown:

- Amazon committed $200 billion, which is bigger than the GDP of most countries.

- Google came in at $175-185 billion.

- Microsoft is tracking $110-120 billion.

- Meta sits between $115 billion and $135 billion.

But for anyone running a business on rented infrastructure, the part that matters came in a BankInfoSecurity report from February 24, 2026: even with spending at record levels, 26% of data center projects got delayed in 2025. The industry leased over 15 gigawatts of capacity last year and almost none of it actually came online, nearly all of it slid to late 2026 and 2027.

And that gap, between what got leased on paper and what physically exists, is exactly where the price pressure comes from.

Power is the bottleneck, not hardware

This one caught a lot of analysts off guard. The thing holding everything back isn’t chips or servers anymore. It’s electricity.

- Gartner predicts power shortages will constrain 40% of AI data centers by 2027.

- Goldman Sachs projects data center power demand growing 15% a year through 2030, ending up at 8% of all US electricity.

- The North American Electric Reliability Corp warned that several grid regions face a higher risk of summer electricity shortages in 2026.

- PJM Interconnection, the grid operator running 13 eastern US states, held its latest capacity auction and came up 6,625 MW short of its reliability target.

That PJM number is not some hypothetical. That’s the grid operator itself telling the market there isn’t enough generation committed to cover what’s coming.

Data center developers who used to pick sites on latency and fiber access are down to one question now, where can I get megawatts? Secondary markets that would never have made anyone’s shortlist five years ago are suddenly in play, purely because they have grid capacity to spare.

For dedicated server customers this lands directly. Providers that locked in power agreements early can hold their pricing steady. The ones scrambling for new capacity, well, now you’re the one paying for that scramble.

The dedicated server market was valued at $20.15 billion in 2024

Maximize Market Research put the global dedicated server hosting market at $20.15 billion in 2024, heading for $80.49 billion by 2032 at an 18.9% CAGR. North America held 40% of that and is expected to grow faster than any other region through 2026.

What’s driving the growth isn’t complicated:

- AI workloads need their own resources. The US Chamber of Commerce reported 58% of small businesses now use generative AI, and running AI automation or chatbots takes dedicated CPU and RAM that shared environments just can’t give you.

- Compliance wants physical isolation. 86% of IT professionals still go dedicated for performance predictability and compliance, according to Liquid Web.

- The noisy neighbor problem is real. When your database sits on hardware nobody else touches, there’s no random slowdown because some other tenant decided 2 AM was the moment for a heavy job.

Dedicated hosting is about 27.9% of the wider web hosting market, and that share sounds modest until you remember the whole market is worth somewhere between $149 and $193 billion depending on which research firm you ask.

For businesses targeting US customers the physics argument stays simple. A server sitting in New York, Dallas, or Chicago gets routing that hosting from outside the country can’t match, latency to North American users stays in single digits instead of the 80-120ms you’d see out of European data centers.

Construction costs hit $11.3 million per megawatt in 2026

JLL’s 2026 outlook has the average global data center construction cost reaching $11.3 million per megawatt this year. For context:

- That’s up from $7.7 million per MW in 2020, a 47% increase over six years.

- And that figure only covers shell and core. Tenant tech fit-out for AI infrastructure can add another $25 million per MW on top of it.

- Between 2020 and 2025 average construction cost grew about 7% a year.

The labor side is getting worse, not better. DataBank says peak crew sizes at major construction sites now hit 4,000-5,000 workers, the population of a small town deployed to build one data center campus. Workers are leaving markets where construction slowed, Arizona for one, where power constraints paused projects, and heading to booming regions like Dallas. That migration pushes wages, per diem, and relocation costs up everywhere at once.

These economics reach the customer eventually. If it costs a provider 47% more to build capacity than it did in 2020, that doesn’t get absorbed forever, it shows up in monthly pricing, in contract terms, or in less availability at the same price point.

Did you know the VPS server Market Crossed $5 Billion in 2025!

What this means if you’re choosing infrastructure right now

The numbers all point one direction. US data center demand is outrunning supply, power constraints are real, construction costs keep climbing, and hyperscaler spending is reshaping the whole ecosystem in ways that won’t settle before 2028 at the earliest.

For businesses renting dedicated server infrastructure, the practical takeaways:

- Lock in pricing where you can. Providers with long-term power agreements and existing capacity are holding cost advantages the late entrants don’t have. Month-to-month price stability matters more now than it did two years ago.

- Location genuinely matters for cost now. Primary markets like Northern Virginia are the tightest. Secondary markets with grid capacity to spare may get you better pricing and faster provisioning.

- The gap between shared and dedicated keeps widening. Shared hosting can’t give you the isolated resources that AI workloads, high-transaction databases, and compliance-sensitive applications need, and that 18.9% growth rate for dedicated is businesses figuring that out at scale.

- Don’t count on US infrastructure costs coming down soon. The 11 GW shortfall, the construction cost climb, the power bottleneck, all of it is structural, not temporary.

The US still has by far the most developed data center ecosystem on the planet. That part is real. But it’s under more pressure than at any point in the last two decades, and the pricing effects are already filtering down into every tier of the market.

References

- JLL, “2026 Global Data Center Outlook,” published March 2026 – https://www.jll.com/en-us/insights/market-outlook/data-center-outlook

- Goldman Sachs, US Data Center Supply and Demand Estimates through 2028, via Visual Capitalist – https://www.visualcapitalist.com/shortage-of-u-s-data-center-capacity-2023-2028p/

- BankInfoSecurity, “Data Center Capacity Crisis Puts 2026 Road Maps at Risk,” February 24, 2026 – https://www.bankinfosecurity.com/data-center-capacity-crisis-puts-2026-road-maps-at-risk-a-30842

- Futurum Group, “AI Capex 2026: The $690B Infrastructure Sprint,” February 2026 – https://futurumgroup.com/insights/ai-capex-2026-the-690b-infrastructure-sprint/

- Data Center Richness, “Hyperscalers Plan $630 Billion in 2026 CapEx,” February 2026 – https://datacenterrichness.substack.com/p/hyperscalers-plan-630-billion-in

- Gartner, Power Shortage Prediction for AI Data Centers by 2027

- DataBank, “Data Center Construction Predictions for 2026,” January 2026 – https://www.databank.com/resources/blogs/data-center-construction-predictions-for-2026/

- Maximize Market Research, “Dedicated Server Hosting Market – Global Industry Analysis and Forecast (2025-2032)” – https://www.maximizemarketresearch.com/market-report/global-dedicated-server-hosting-market/109734/

- US Chamber of Commerce, SMB AI Adoption Report, 2025

- Programs.com, “Measuring the Data Center Boom: Facts and Statistics (2026)” – https://programs.com/resources/data-center-statistics/